Back To All Resources

Articles

The step-by-step process of Supplier and Payment Terms Analysis

September 23, 2021

Read time:

5 min

September 23, 2021

The supplier and payment terms analysis can be accomplished within a few minutes using an automated solution such as the ADA Platform or between two and six weeks, using the conventional manual way. There are further dependencies like the number of suppliers being analyzed and the level of details that will significantly affect the cost and time to complete manually which would not be impacted by the use of the automated digital solution.

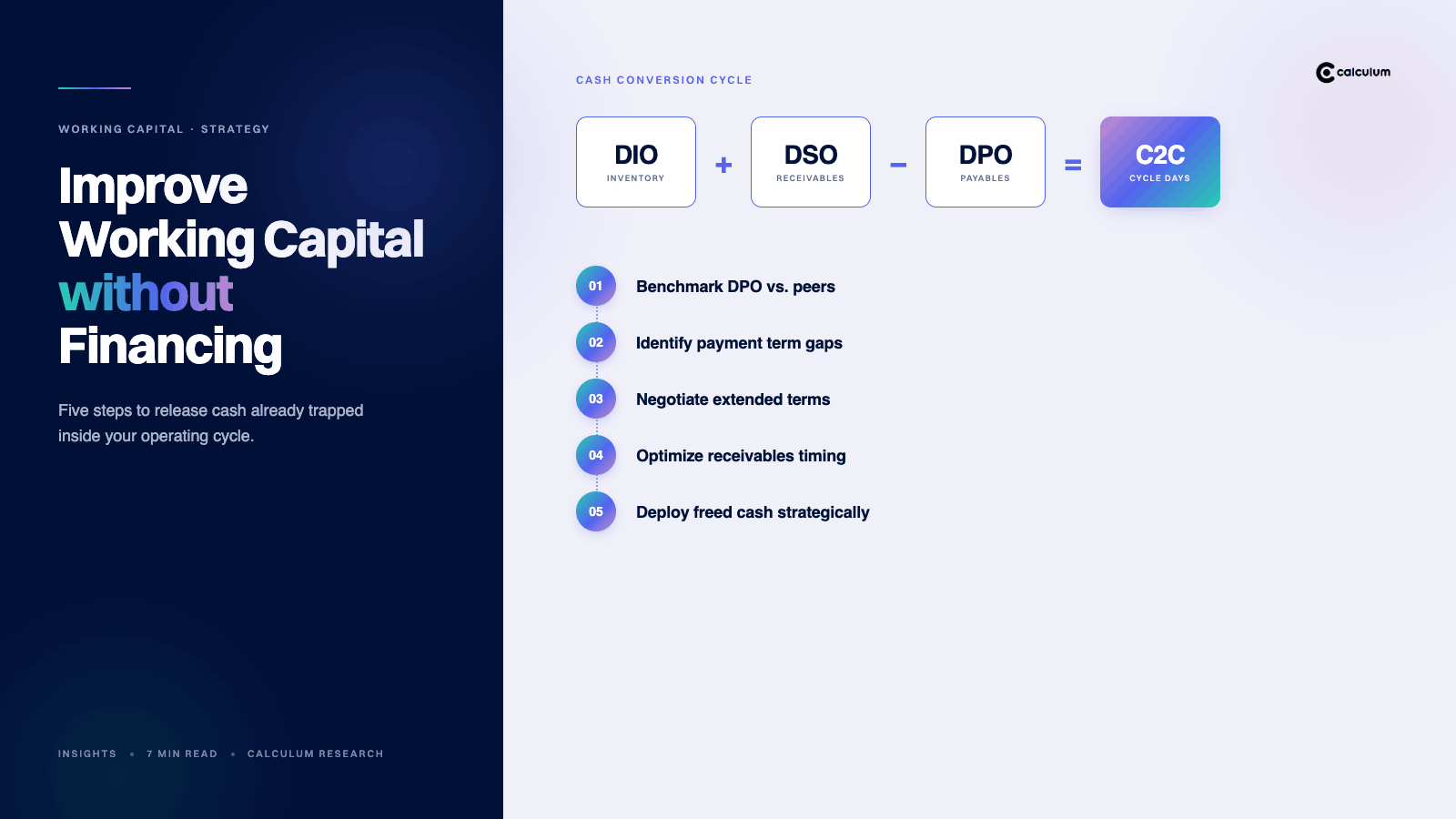

Before starting the analysis, it is important to review the specific goals of the buying organization. Targets can include cash flow, cost savings, expected returns through cash discounts, or specific C2C(Cash to Cash Cycle) goals as well as the respective timelines. Usually, the analysis consists of the following process steps:

The supplier and payment terms analysis starts with the buying organization providing its spend data – in most cases, an Excel or CSV file with data extracted from its ERP (Enterprise Resource Planning)system. The spend data should include the following details:

Other information, which can be useful for the analysis is the supplier's identification number used by the buyer, the category of goods purchased from a supplier, the ERP system used by the buyer per supplier, detailed supplier address, number of years of supplier-buyer relationship, and the date of the next contract renewal or contract renegotiation.

In most cases, term optimization programs that are unsuccessful are the ones that have adopted a scattergun approach - negotiating payment terms with every supplier without any focus. Usually, companies have tens of thousands of suppliers, and therefore it makes sense to identify the ones that will have the biggest impact and focus on optimizing terms with these trading partners.

When companies begin to review their suppliers, they are often surprised at the number of suppliers that they have. They usually are off by order of magnitude. The best approach is to concentrate on key strategic suppliers first by applying the 80-20 rule - focusing on the largest 20% suppliers responsible for 80% of the total spend. Focusing on important suppliers allows implementing a terms optimization program in a systematic and efficient way.

Usually, the spend and supplier information received from the buyer comes from different sources and is not ready to perform a proper analysis. Sometimes the data elements such as supplier names, payment terms, and other information have to be normalized using common language and terms. This also includes data cleansing and standardizing spelling.

Cleansing means that all references to one particular company, such as IBM, are consistent, even though it may be named in numerous ways such as International Business Machines Corporation, IBM Corp, IBM US, etc. The same applies to payment terms where different codes and names are used by the buying organization such as PT 35, 35, CD35, 3%, 35 days, etc. as well as country names such as DE, Germany, Deutschland, etc.

Once the spend data is cleaned, reviews in terms of concentrations per different factors are performed to focus on the top suppliers. Spend data can be classified across all categories, divisions, spend volume, credit rating, industries, countries, or other supplier groups such as per buying entity, certain spend, currency, current payment terms, geographies, specific categories, or buyer's ERP systems.

This is an important step because consistently cleaned data allows for more accurate classification metrics which gives the company more arguments during negotiations or decision-making situations which ultimately positively influences the company’s working capital and revenue.

The step of data enrichment can be a long process as it takes into account collecting data from different external data sources such as for example CapitalIQ, Factset, Dun & Bradstreet, and proprietary databases to increase the depth of information in the analysis. The analysis of each supplier can be enriched with information such as:

Where the supplier belongs to a wider organization, the data is collected for the parent company, and adjustments are made to consider the level where the supplier stands within the overall organization. Sometimes, little or inaccurate data is available, especially for smaller suppliers or companies located outside OECD countries. In these cases, an estimate has to be applied based on market experience or the market itself. This is an important step, and the experience of the analysis platform reflects the accuracy and quality of the analysis.

Based on the enriched data, every single supplier is scored in order to identify which trading partner would be most likely to accept the new payment terms, cash discounts, or join a working capital financing program such as Supply Chain Finance. The supplier scoring includes the following:

Depending on the supplier's location, the DSO might also be distorted. For example, a European-based company would include VAT in its sales figures, which would provide a different DSO value if the same company would be based in the US, where there is no VAT.

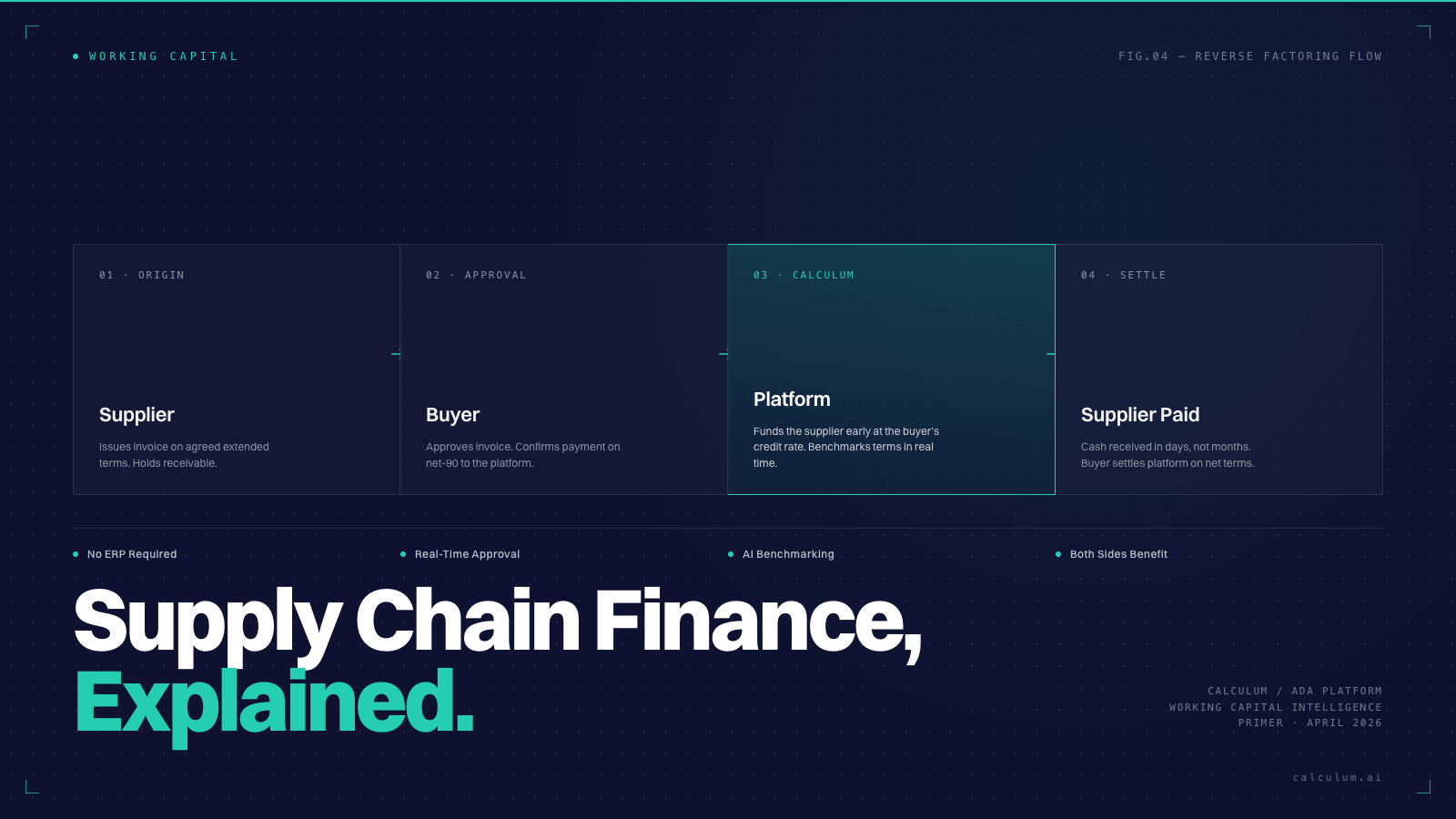

Based on the supplier scoring and payment terms analysis, the next step is to calculate the opportunity for the buyer to optimize payment terms to improve working capital or generate additional returns by offering self-funded early payment terms to suppliers.

There are multiple opportunities to find ways toimprove payment terms or gain additional discounts. Some of the arguments, which are used in the calculation and help procurement with the negotiation areto capture additional discounts by comparing the supplier's cost of funds withthe proposed discounts.

This explains, which suppliers could be converted from standard payment discount terms, that the buyer is unable to effectively take advantage of, to dynamic terms. There are estimates that show that only8-12% of supplier invoices contain discount terms, which reveals a lot of opportunities to reduce COGS (Cost of Goods Sold). On the other side, if the buyer is looking more to extend payment terms, the analysis can reveal opportunities to convert cash discounts to net terms.

For example, a supplier offering 2%, 10 net 30payment terms - offering a 2% discount for payment within ten days instead of30 days - essentially, the supplier is paying 2% of the invoice value for accelerating payment by 20 days. That equates to an effective annual interest rate of approximately 36%. Based for example on an annual Supply Chain Finance or Reverse Factoring rate of 1%, the analysis can reveal an opportunity to extend terms from net 30 to 50 days without the supplier being worse off.Another focus is to identify opportunities in terms of different standards, including:

The article belongs to a three part series. The focus of the other two articles in thisseries is:

.png)

.png)

.jpeg)

.png)