Back To All Resources

Articles

The 60-Day Hard Cap: Why the UK’s New Payment Reform Is a Working Capital Wake-Up Call

April 7, 2026

Read time:

5 min

April 7, 2026

The UK government has made its direction clear: late payment reform is moving from encouragement to enforcement. In its March 2026 response to the Time to Pay Up consultation, the government confirmed its intention to introduce what it describes as the most significant legislation on late payments in over 25 years, and one of the strongest frameworks across the G7.

At the center of the package is a proposed hard 60-day cap on payment terms in the UK is being introduced in transactions where large businesses pay smaller suppliers. Just as important, the long-relied-on grossly unfair standard, which previously allowed extended terms under certain conditions, is being removed.

This is not just a technical adjustment. It is a structural shift in how working capital is distributed across the UK B2B economy.

The proposed 60-day limit is only one element of a broader enforcement framework designed to reshape payment behavior.

The UK government intends to:

Together, these measures signal a clear shift: late payment is no longer a commercial negotiation issue, it is becoming a regulatory risk.

For treasury, procurement, and finance teams, the implications are immediate, even before formal implementation.

The most direct impact is tenor compression.

Supply Chain Finance (SCF), receivables finance, and factoring programs often rely on longer payment cycles: 90, 120, or even 180 days. A regulatory cap at 60 days will require these structures to be reassessed and, in many cases, redesigned.

This does not eliminate liquidity needs, but it fundamentally changes:

At a system level, this reform introduces a forced redistribution of working capital. Larger buyers operating on extended terms will be required to release liquidity back into the supply chain, particularly to smaller suppliers.

Importantly, this shift is not accidental. The government has made clear that some disruption to larger businesses’ working capital positions is an intentional outcome of the reform.

While the 60-day cap is central, it is not universal across all B2B transactions.

The framework is expected to include targeted exemptions, such as:

Additionally, elements such as invoice verification processes may still influence when payment obligations formally begin.

This means one thing: The challenge is not just compliance, it is interpretation.

Companies that oversimplify the regulation risk either overcorrecting commercially or underestimating their exposure.

This reform transforms payment terms from a negotiation lever into a regulated parameter.

In this environment, companies must answer critical questions with precision:

Without clear, data-backed answers, decision-making becomes reactive, and risk increases.

As payment terms become more regulated, the ability to act strategically depends on visibility.

Organizations will need to move beyond:

…and toward:

In a 60-day world, the question is no longer how to extend terms, but where optimization is still possible within the rules.

This is where Calculum’s approach becomes particularly relevant.

When regulatory pressure compresses payment terms, the competitive advantage shifts toward companies that can identify:

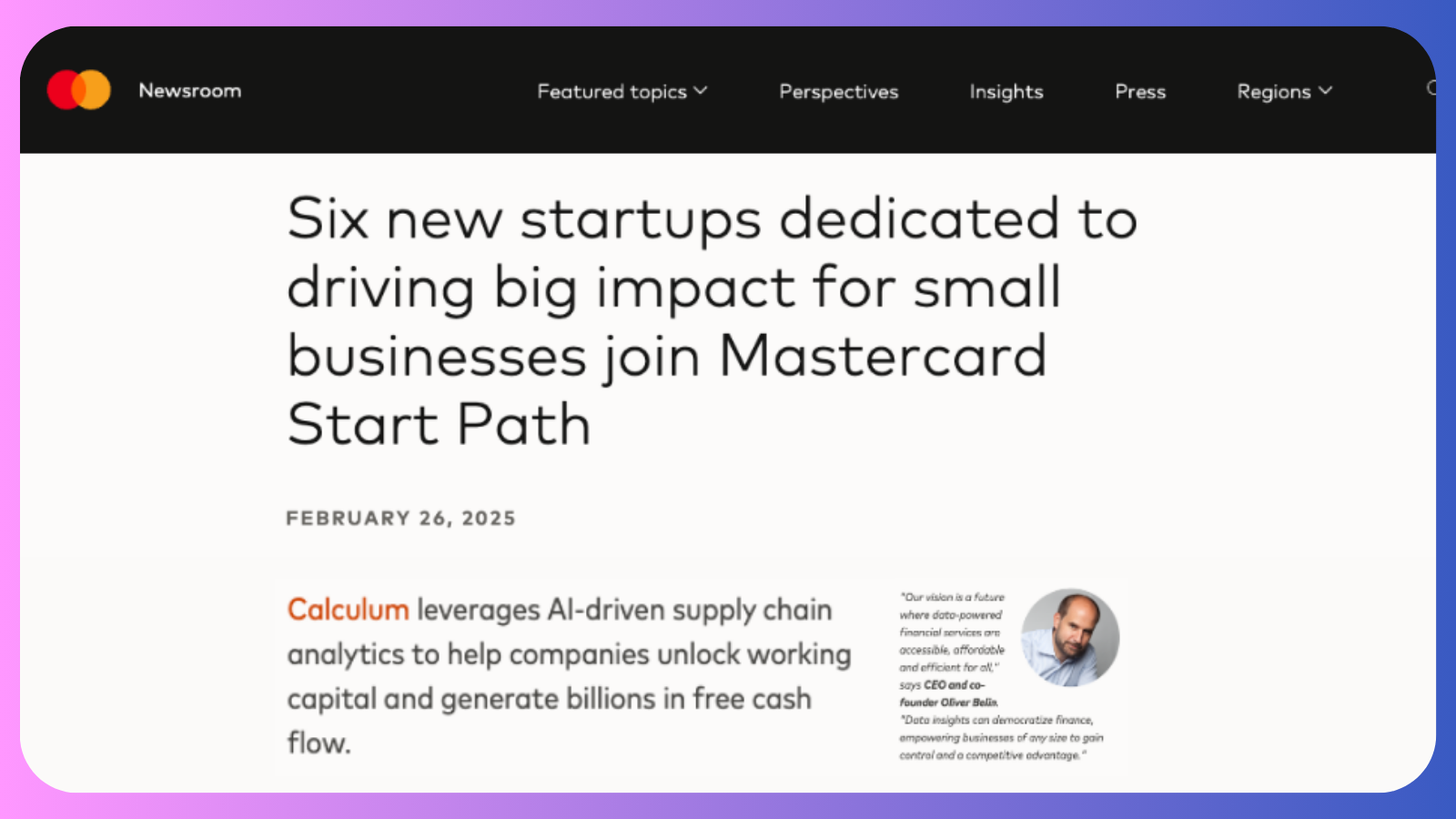

Calculum provides treasury and procurement teams with data-backed visibility across the financial supply chain, including payment terms benchmarking, supplier financial profiles, and negotiation intelligence.

Powered by one of the largest payment terms databases globally covering over 7.1 million companies and $3.3 trillion in analyzed spend, Calculum enables organizations to replace guesswork with precision and make informed decisions in an increasingly regulated environment.

The UK’s late payment reform is not just a regulatory update, it is a structural shift in how working capital is managed.

For some organizations, it will be a compliance challenge. For others, it will be a catalyst to rethink their entire financial supply chain strategy.

The difference will come down to one factor: Who has the data to act with precision and who does not.

For full details on the proposed reforms, you can review the official UK government announcement here.

.png)

.png)

.jpeg)

.png)