Payment terms have always been at the core of any B2B commercial negotiation. They sit at the intersection of procurement, supply chain management, and treasury.

A well-structured payment terms optimization program, supported by the latest market intelligence and with an option to offer Supplier Financing, also called Supply Chain Finance, is one of the most powerful working capital levers available to any enterprise when looking at their vendor terms.

In 2026, the environment around that negotiation is changing. Governments across Europe are enacting legislation that regulates payment terms, targets late payment, and mandates digital transparency. These changes are real, and they deserve serious attention from CPOs, Treasurers, and CFOs operating across multiple jurisdictions.

But the conventional reading of this regulatory wave is wrong. The narrative that extended payment terms and Supply Chain Finance (SCF) are under threat, that buyers are losing leverage, and that the era of payment terms negotiation is drawing to a close misreads both the legislation and the opportunity.

Most of these regulations target one specific problem of the current system: late payment, meaning the failure to pay within agreed terms. They do not target, and in many cases explicitly preserve, the commercial freedom to negotiate extended terms, provided those terms are formal, transparent, and backed industry benchmarks.

For the procurement category managers who benchmark payment terms with precision, negotiate from a position of market data, and in some cases back extended terms with a well-structured SCF program, the regulatory environment of 2026 is not a headwind. It is a tailwind. Transparency rewards the prepared.

The Most Important Distinction in Global Payment Policy

Before examining any specific legislation, one distinction must be established clearly, because its confusion distorts almost every narrative on this topic.

Late payment is paying after the agreed contractual due date. This is what regulators are targeting. It is a breach of contract, a cash flow risk for suppliers, and a systemic financial problem. Late payment regulations, with some times introducing late interest rate fees are designed to eliminate this specific failure.

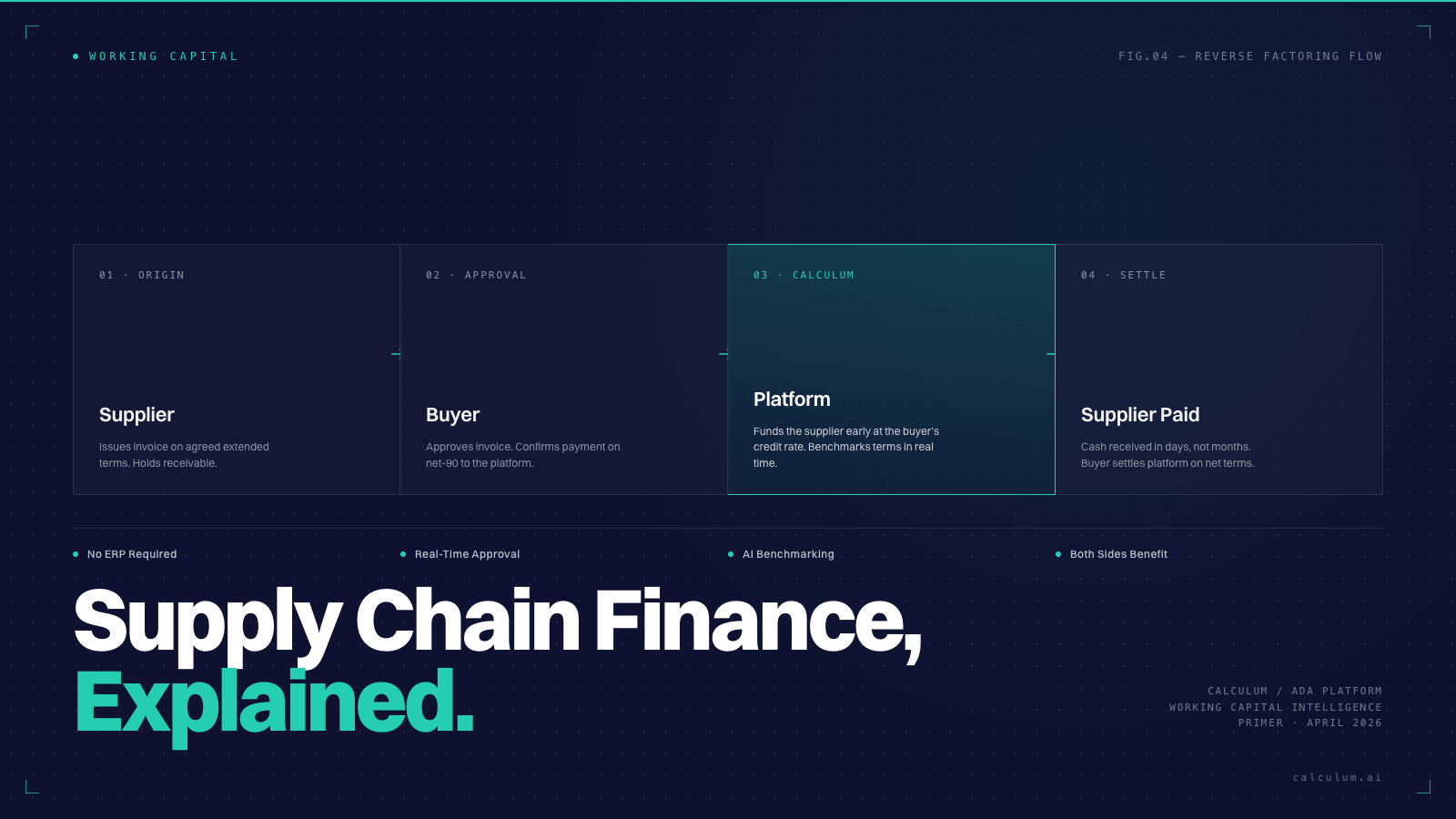

Long payment terms are formally negotiated, commercially agreed payment terms such as 60 days. This is a legitimate working capital tool. When backed by market benchmark data and finance programs that give suppliers access to early payment at fair cost, long payment terms can be mutually beneficial.

These two concepts are fundamentally different, and conflating them is a consequential analytical error in the current conversations about payment term regulation. A company with Net 90 terms that pays on day 88 is doing something entirely different from a company with Net 30 terms that pays on day 75. The second is what most regulators are attacking. The first is sophisticated treasury management.

The question for CPOs and Treasurers in 2026 is not how to comply with tighter payment windows. It is how to use the new regulatory transparency to negotiate better terms, structure stronger SCF programs, and identify where working capital is being left on the table. The answer requires benchmarks, AI, and data, not a defensive posture.

A Region-by-Region Picture

The full report maps the 2026 regulatory landscape across six key markets: Belgium, Switzerland, the Netherlands, the United Kingdom, France, and Germany.

Each country tells a different story. Belgium has shifted from flexibility to enforcement, combining strict statutory caps with mandatory e-invoicing through the Peppol network. Switzerland remains liberal, relying on the principle of Freedom of Contract under the Swiss Code of Obligations and offering significant room for strategic negotiation. The Netherlands has built one of the most prescriptive frameworks in Europe, with payment caps tied directly to company size classification. The United Kingdom is closing the grossly unfair loophole that previously allowed buyers to justify 90-day terms, with reforms integrated into the Procurement Act 2023 and the Fair Payment Code. France is widely considered the most stringent of European payment regulations, with its 2026 Finance Bill introducing real-time digital transparency. Germany has moved from a freedom of contract model toward a presumptive fairness model, where the burden of proof for long terms rests heavily on the buyer.

For each country, the full report details the historical context, current domestic rules, cross-border implications, late payment penalties, and the specialized exceptions that procurement teams can still leverage to find strategic breathing room within the law.

Why 2026 Is the Right Time to Negotiate

Reviewing the regulatory landscape across these markets as a constraint on payment terms strategy would be the wrong response to the evidence. The right response is to recognize that the environment is creating conditions under which informed, data-driven buyers with well-structured term optimization initiatives, including SCF, are more advantaged.

The single most important effect of the regulatory changes across this region, whether CSRD G1-6 disclosure in the EU, new payment terms regulations in the UK, or e-invoicing audit trails across multiple jurisdictions, is the creation of market transparency around payment behavior. In an opaque market, every buyer negotiates from assumptions. In a transparent market, every buyer negotiates from data.

The category manager who knows what payment terms peers are achieving in European manufacturing, in UK retail, in Swiss agriculture, holds a negotiating advantage that did not exist a few years ago. The transparency being driven by regulation is accelerating the normalization of payment terms benchmarking. Companies that invest in that intelligence and act on it will gain working capital positions that less data-driven competitors cannot match.

The companies that treat payment terms as a strategic financial lever rather than an afterthought will emerge from this environment with materially stronger working capital positions.

.png)

.png)

.jpeg)

.png)