Back To All Resources

Articles

What Is Supply Chain Finance and How It Works

May 7, 2026

Read time:

8 min

May 7, 2026

Supply chain finance (SCF), also known as supplier finance, payables finance, or reverse factoring, is one of the most powerful working capital tools available to large enterprises, yet it is also one of the most consistently misunderstood. The confusion usually begins with terminology: supply chain finance is conflated with factoring, with early payment programs, with reverse factoring, and occasionally with trade finance in general.

While Supply Chain Finance (SCF) is a powerful tool for injecting liquidity into the supply chain, its success depends entirely on the strength of the underlying data. At Calculum, we provide the payment terms intelligence and benchmarking needed to optimize terms before financing begins, seamlessly integrating with and empowering the broader SCF ecosystem.

This guide defines supply chain finance precisely, explains how the most common structures work step by step, and connects the mechanics to the working capital outcomes that CFOs and Treasurers are seeking when they implement these programs. For context on how supply chain finance fits into the broader history of trade finance, see our article on the evolution from factoring to open account trade.

Supply chain finance is an umbrella term covering a range of financing arrangements that optimize the timing of cash flows in a supply chain. In the context most relevant to large corporate buyers, it refers specifically to buyer-led financing programs that allow suppliers to receive early payment on their approved invoices, typically at a financing rate linked to the buyer's credit rating rather than the supplier's.

The core value proposition is asymmetric: the supplier gets access to liquidity at a rate they could not achieve independently, and the buyer extends their payment terms without imposing a cash flow burden on the trading partner. A well-structured supply chain finance program creates a genuine win-win that makes extended payment terms commercially sustainable.

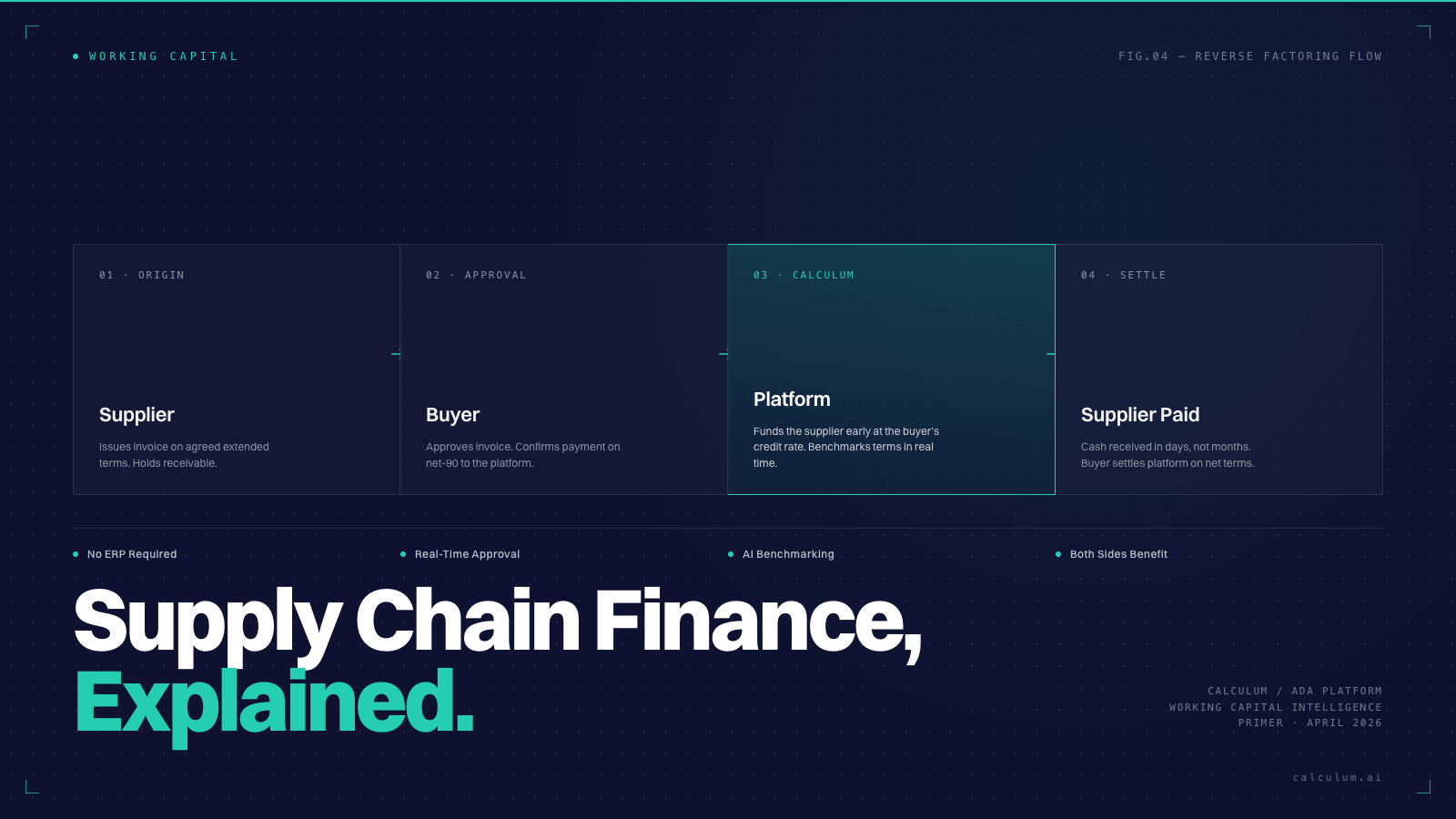

The most widely used supply chain finance structure is reverse factoring, also called approved payables financing or confirmed payables. The process follows four steps:

The buyer-led structure described above. Triggered by buyer invoice approval, voluntary for the supplier, typically bank or institutional-funded. The most common structure for large corporate supply chain finance programs.

A self-funded program where the buyer uses their own cash to offer early payment to suppliers in exchange for a discount. The buyer captures the discount as a return on short-term cash deployment. Dynamic discounting is most valuable when the buyer has excess liquidity and the suppliers offer attractive discount rates relative to money market alternatives.

In factoring and invoice financing, the supplier sells their receivables to a financier without buyer involvement or approval. This is distinct from reverse factoring in that the buyer's credit rating does not determine the financing rate, and the buyer has no role in initiating the program. It is the most common form of trade finance for SMEs but is less relevant to large corporate supply chain finance strategy.

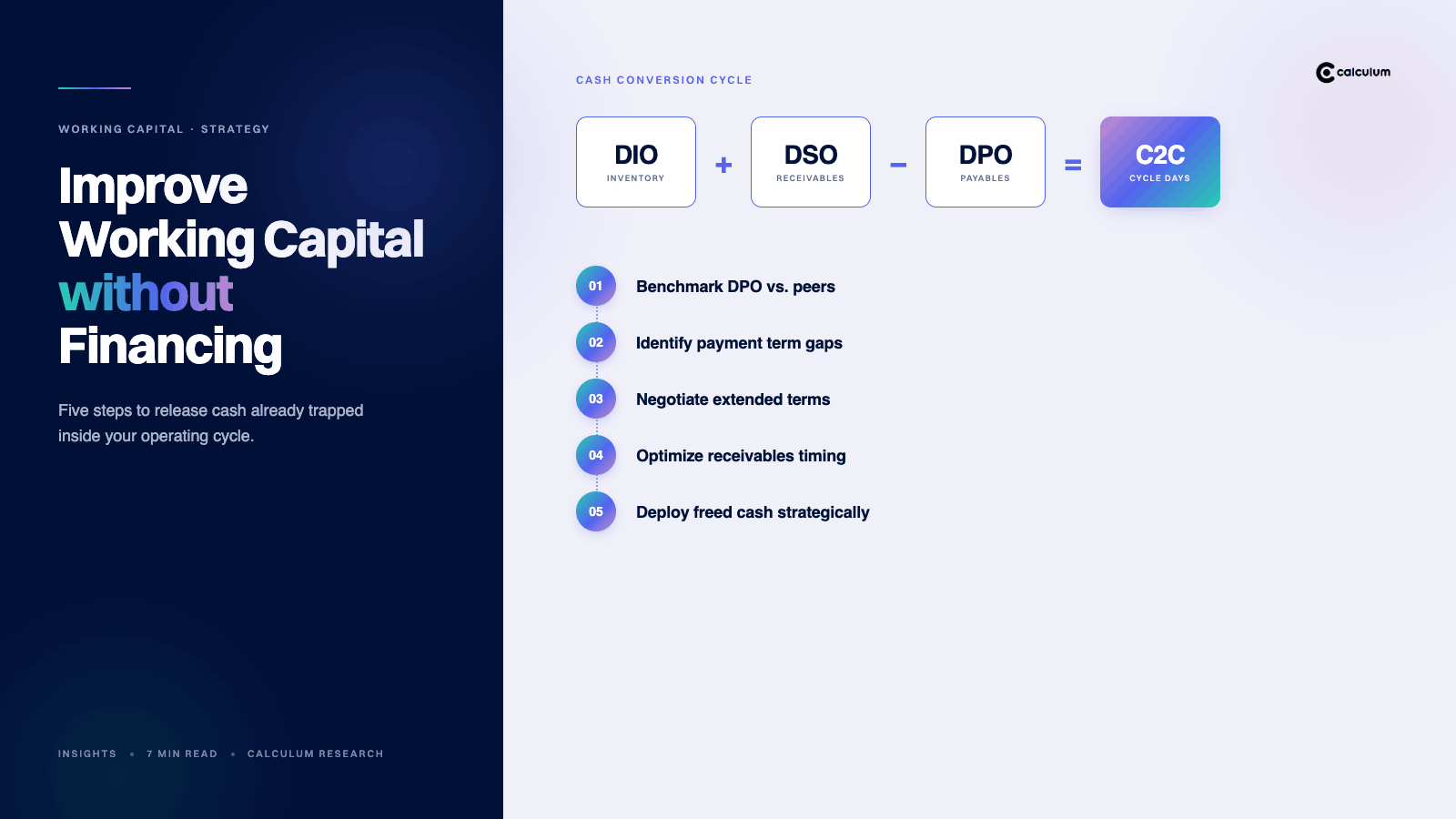

Supply chain finance programs are not primarily financing products. They are working capital optimization enablers. Their strategic value is in what they make possible: the extension of payment terms from buyers to trading partners without damaging the supplier's cash position.

Without supply chain finance, extending payment terms from 30 to 60 days with a strategic trading partner imposes a cash flow cost on that supplier. If the supplier cannot absorb that cost, the negotiation fails or the relationship suffers. With supply chain finance, the supplier has voluntary access to early payment at competitive rates, meaning the effective impact on their cash position is positive even as the buyer's DPO improves.

To understand how to sequence payment terms optimization and supply chain finance as part of a broader working capital program, see our guide on how to improve working capital without financing.

The quality of a supply chain finance program is determined by five factors:

Calculum's payment terms intelligence platform supports supply chain finance program design as part of the payment terms optimization workflow, identifying which supplier tiers and categories are the best candidates based on spend concentration, current terms, and market benchmarks. No ERP integration required. Get started to see what a data-driven program looks like for your business.

Factoring is supplier-initiated: the supplier sells their receivables to a financier to access early cash, regardless of buyer involvement. Supply chain finance is buyer-initiated: the buyer anchors the program using their own credit rating, allowing trading partners to receive early payment at significantly lower rates than they could access independently.

Properly structured supply chain finance programs do not create additional debt for the buyer. The buyer is simply paying their existing trade payables on the agreed due date, with a financier intermediating the timing for the supplier's benefit.

In supply chain finance (reverse factoring), a third-party financier provides the early payment capital at a rate tied to the buyer's credit rating. In dynamic discounting, the buyer uses their own cash to provide early payment in exchange for a discount. The right choice depends on whether the buyer has excess liquidity and the relative attractiveness of discount rates.

Supply chain finance and payment terms strategy are most effective when designed together. Supply chain finance allows buyers to extend payment terms with strategic trading partners without imposing a cash flow burden on those suppliers, making extended terms commercially viable for both parties.

.png)

.png)

.jpeg)

.png)